Challenges facing superannuation members

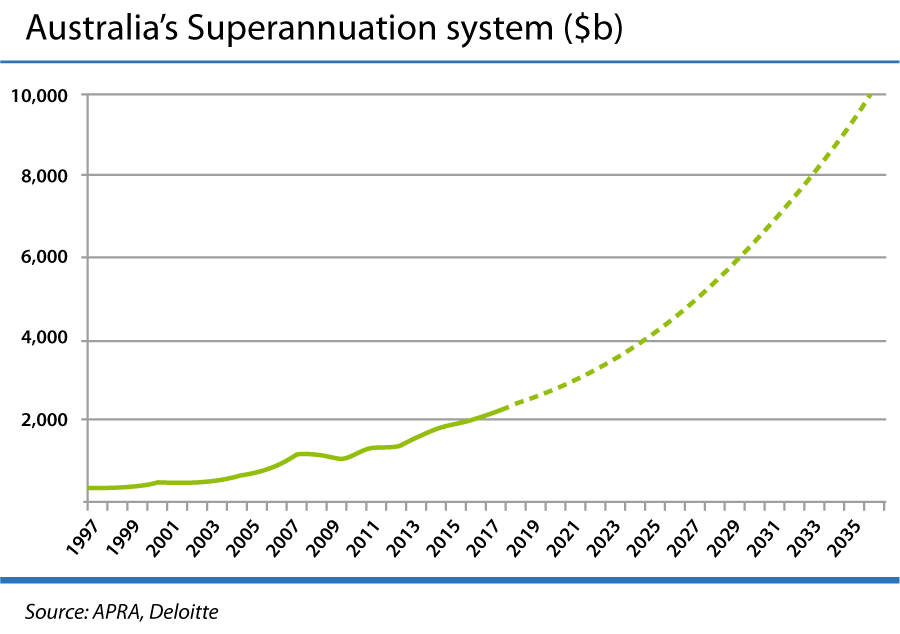

In the current landscape the value of Australian superannuation assets is nearing $3 trillion. That number is projected to soar to $10 trillion over the next two decades, ranking Australia as one of the world leaders in pension size and sophistication.

by Benny Berkowitz

In the current landscape the value of Australian superannuation assets is nearing $3 trillion. That number is projected to soar to $10 trillion over the next two decades, ranking Australia as one of the world leaders in pension size and sophistication.

More and more superannuation members are taking advantage of the flexibility and control that comes with running a self-managed superannuation fund (SMSF) rather than a traditional wholesale/retail superannuation fund. Conversely, with the political turmoil and uncertainty as well as a raft of new laws introduced over recent years, a new set of challenges impact the superannuation sphere.

Proposed changes to the imputation credit rules

One of the most common SMSF investments are listed shares which typically pay income to shareholders in the form of dividends. Often these dividends will have tax credits attached called imputation credits (also known as franking credits) that effectively refund the shareholder any company tax paid on that dividend income. This in essence avoids double taxation in the hands of the shareholder (i.e. to prevent both the company and shareholder paying tax on the same income).

At present, imputation credits are currently refundable to those in account-based pension phase (with assets under the $1.6 million pension cap).

Leader of the Opposition Bill Shorten has proposed that imputation credits from dividends paid directly by companies, or indirectly via other pass-through entities, will no longer be fully refundable for superannuation funds and individual investors.

Therefore, those most affected will be income recipients who rely on their imputation credit refunds. Take the example of a retiree with a $300,000 share portfolio in their SMSF and no other assets. These shares might receive approximately $5700 of imputation credits which are then refunded as cash. If the imputation credit ban were enacted, the SMSF would lose that imputation credit refund and experience substantial decline on the cash return earned by that share portfolio.

There has been much conjecture about whether the ban could possibly be passed (if Labor wins the next election) and if so, what the potential wider effects could be. I have heard from numerous clients who have suggested that they would consider selling their share portfolios to find alternate investments if they were no longer entitled to a refund of their imputation credits.

Transfer balance cap – $1.6m pension limit

The transfer balance cap was introduced on July 1, 2017 to limit the amount a superannuation member can keep in an account-based pension and receive concessional tax treatment. In the past, there was no limit to the amount a member could have in an account-based pension, with the earnings (including capital gains) being tax free on assets supporting that pension account.

From July 1, 2017, a $1.6 million pension limit was implemented with earnings from assets above the $1.6 million limit being taxed at 15 per cent (or 10 per cent for capital gains on assets held 12 months or more).

The $1.6 million pension limit is an aggregate limit per superannuation member regardless of the number of account based pensions they hold.

Taxing of TRIS income

Transition to retirement income streams (TRIS) were introduced to assist superannuation members gradually move to retirement by accessing a limited amount of superannuation in the form of a pension.

Previously, income earned by assets supporting a TRIS balance was tax free (including capital gains), similar to income earned in an account-based pension. However, effective July 1, 2017, earnings from assets supporting a non-retirement phase TRIS are now taxed at 15 per cent (or 10 per cent for capital gains on assets held 12 months or more) regardless of the date the TRIS commenced.

Events-based reporting

The new pension limits outlined earlier necessitate prescriptive reporting requirements. Superannuation advisers who prepare the relevant submissions will likely charge for this service adding to the overall administration costs of the fund.

Relying on Google

With vast amounts of information readily available online, some SMSF trustees are turning to internet research in place of seeking professional advice.

Due to the increased complexity of the superannuation rules, this could invariably lead to trustees taking measures that might result in a superannuation breach which could be costly or difficult to rectify. SMSF advisers have the task of engaging with their SMSF trustee clients to ensure that they have the relevant knowledge and advice to adequately run their SMSFs at a price point that is not prohibitive.

Reduction in contribution caps

The concessional (before tax) superannuation contribution annual cap has been reduced to $25,000 and the non-concessional (after tax) contribution annual cap has been reduced to $100,000.

Many superannuation members were relying on previous higher caps to enable them to build appropriate superannuation balances to allow them to comfortably self-fund their retirement. These lower contribution limits could in turn effect decision-making when it comes to downsizing the family home and retiring from gainful employment.

Division 293 tax

Superannuation is a concessionally taxed environment and in 2012 the government introduced an extra 15 per cent tax on the superannuation contributions of high income earners if their income and superannuation contribution combined were greater than $300,000.

Effective 1 July 2017, this income threshold was reduced to $250,000 which surely will have an increased impact on trustees deciding whether to make voluntary concessional contributions.

Conclusion

The government instituted compulsory superannuation in the early ’90s. There was a real fear that the ageing population would result in increased age pension payments that would place an unaffordable strain on the Australian economy. Fast-forward to 2018 and we now have one of the most progressive and advanced retirement systems in the world.

As our superannuation system marches forward, the rules and laws have also grown in complexity. Managing and understanding superannuation is key to ensuring that we are able to build necessary superannuation balances that can self-fund our retirement.

Disclaimer

Important: This is not advice. Readers should not act solely on the basis of the material contained in this article. Items herein are general comments only and do not constitute or convey advice per se. Also changes in legislation may occur. We therefore recommend that formal advice be sought before acting in any of the areas. This article is issued as a helpful guide only.

It is the responsibility of the taxpayer to ensure their records are accurate and complete and particularly, that all income has been included and that all claims can be substantiated. The ATO has substantially increased penalties for omitted income and incorrect claims arising from false or misleading statements of facts.

This article refers to Australian taxpayers solely.

Benny Berkowitz is the director of

Chi Berkowitz Partners.

comments